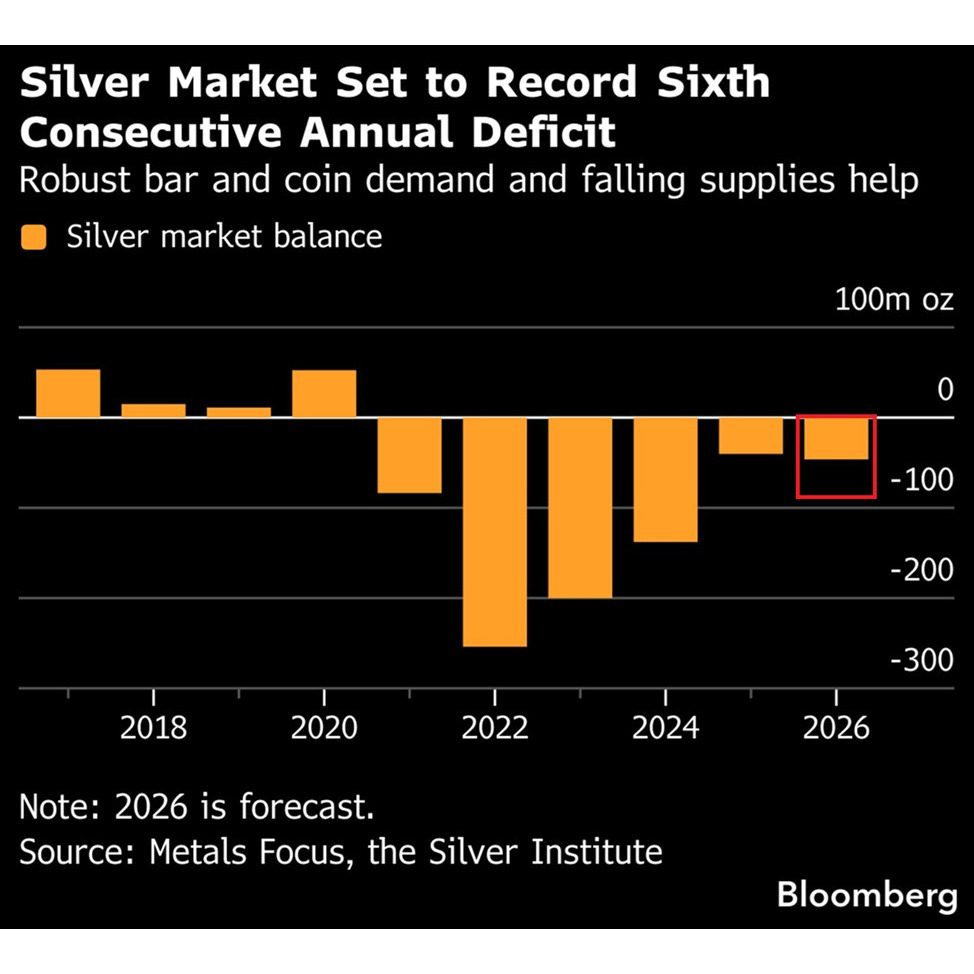

The silver market is heading for a 6th consecutive annual structural deficit:

The global silver deficit is projected to widen +15% YoY in 2026, to 46 million troy ounces.

Since 2021, global silver stocks have been depleted by a cumulative 762 million troy ounces, raising the risk of another liquidity crunch in physical silver markets.

This comes as industrial silver fabrication is estimated to fall -3% YoY to a 4-year low, with the Iran War weighing on global growth and threatening further demand losses.

Coin and bar demand is expected to rise +18% YoY, supported by a recovery in US purchases, partially offsetting the industrial weakness.

Meanwhile, total global silver supply is projected to decline -2% YoY, as miners pull back on production commitments made during last year's price surge.

The silver market has almost never been this tight.

The global silver deficit is projected to widen +15% YoY in 2026, to 46 million troy ounces.

Since 2021, global silver stocks have been depleted by a cumulative 762 million troy ounces, raising the risk of another liquidity crunch in physical silver markets.

This comes as industrial silver fabrication is estimated to fall -3% YoY to a 4-year low, with the Iran War weighing on global growth and threatening further demand losses.

Coin and bar demand is expected to rise +18% YoY, supported by a recovery in US purchases, partially offsetting the industrial weakness.

Meanwhile, total global silver supply is projected to decline -2% YoY, as miners pull back on production commitments made during last year's price surge.

The silver market has almost never been this tight.